Pickle Bookkeeping wants to help you achieve financial success

More than 30 years of experience – Restaurant and bar industry experts

Personalized products – Meeting the needs of your establishment

High customer retention rates – Clients with history of 25+ years

Attuned to Texas needs – Clients in Austin, Houston, Dallas, Fort Worth, San Antonio, and surrounding areas

Your business is our business

We work with you directly to deliver what you want and on your terms, with services that include:

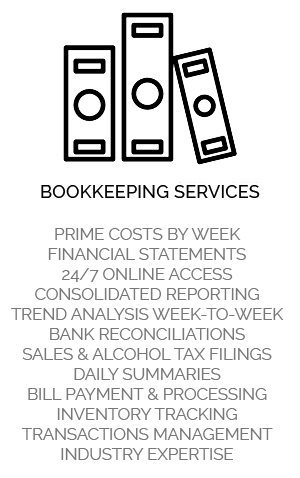

Bookkeeping

Payroll

Business Analytics

Bill Payment

24/7 Online Access